Federal Reserve policy is back in the spotlight, and for good reason. Interest rates, inflation, the Fed’s balance sheet, and the direction of monetary policy all influence markets—especially bonds, housing, lending conditions, equity valuations, and investor sentiment.

The larger question is whether the U.S. is moving toward a less interventionist Federal Reserve, and what that could mean for the economy and portfolios.

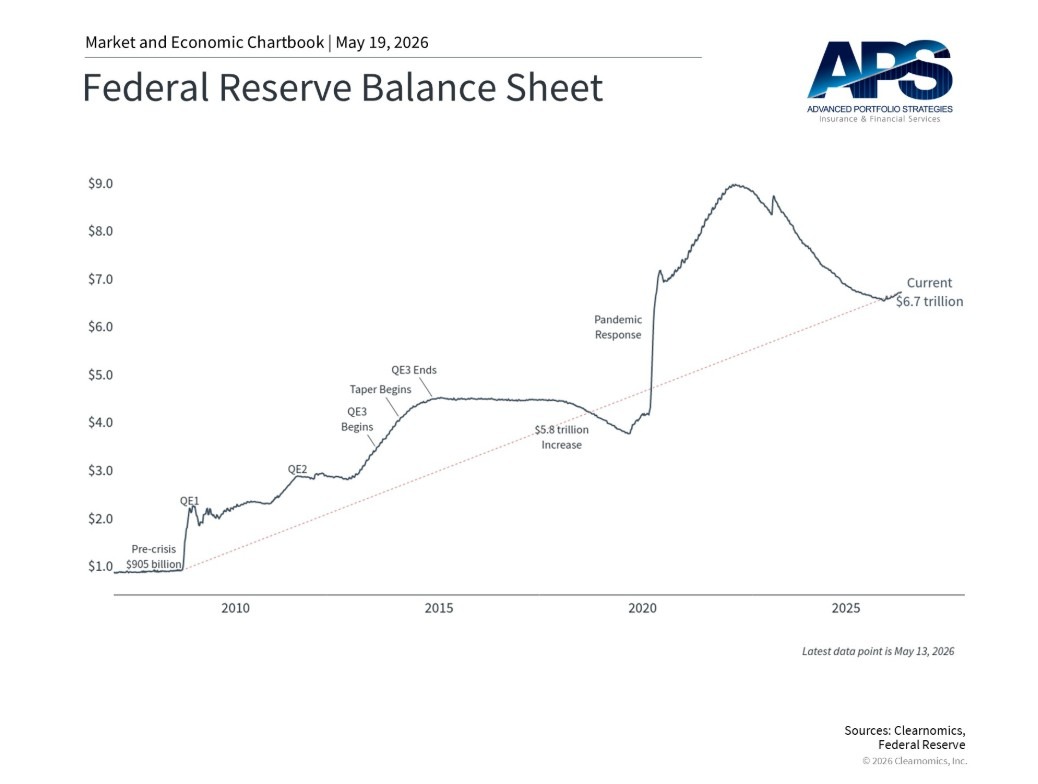

For many years, markets operated with the expectation that the Fed would step in aggressively whenever financial conditions tightened. Quantitative easing, near-zero interest rates, and a significantly larger Fed balance sheet helped stabilize markets during periods of crisis. Those policies may have been necessary at the time, but they were not cost-free.

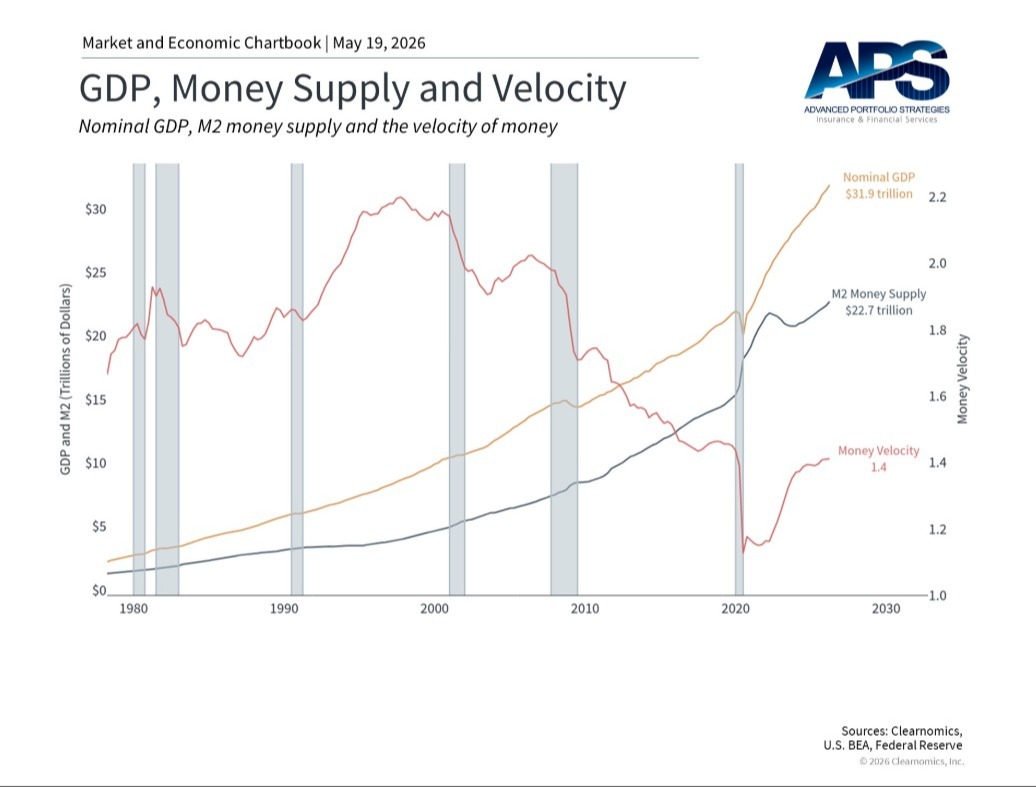

When the price of money is held artificially low for long periods, it can distort the way capital is allocated. Investors may take more risk than they otherwise would. Companies may borrow too cheaply. Asset prices may rise in ways that are not fully supported by underlying cash flows. And weaker business models can survive longer than they should because capital remains abundant and inexpensive.

That matters because interest rates are not just a policy tool. They are also a pricing mechanism. They help determine which investments are attractive, which projects deserve funding, and how investors should be compensated for risk.

A more restrained Fed could, in theory, help restore credibility to the market pricing of capital. That would mean less reliance on emergency-style intervention, a smaller role for the Fed in shaping asset prices, and a greater emphasis on market discipline. Over time, that could be healthy for the economy, even if the transition creates volatility.

But there are also risks. A less interventionist Fed does not automatically mean a smoother market environment. If inflation remains sticky, rates may need to stay higher for longer. If the Fed reduces its balance sheet too aggressively, liquidity conditions could tighten. And if markets have become accustomed to easy money, even a sensible normalization process can feel disruptive.

This is the tension investors should understand. A Fed that restores discipline to capital markets may be good for long-term economic health, but it may also expose areas of the market that were overly dependent on cheap money. That includes highly leveraged companies, speculative growth stocks, parts of commercial real estate, and borrowers that need to refinance at higher rates.

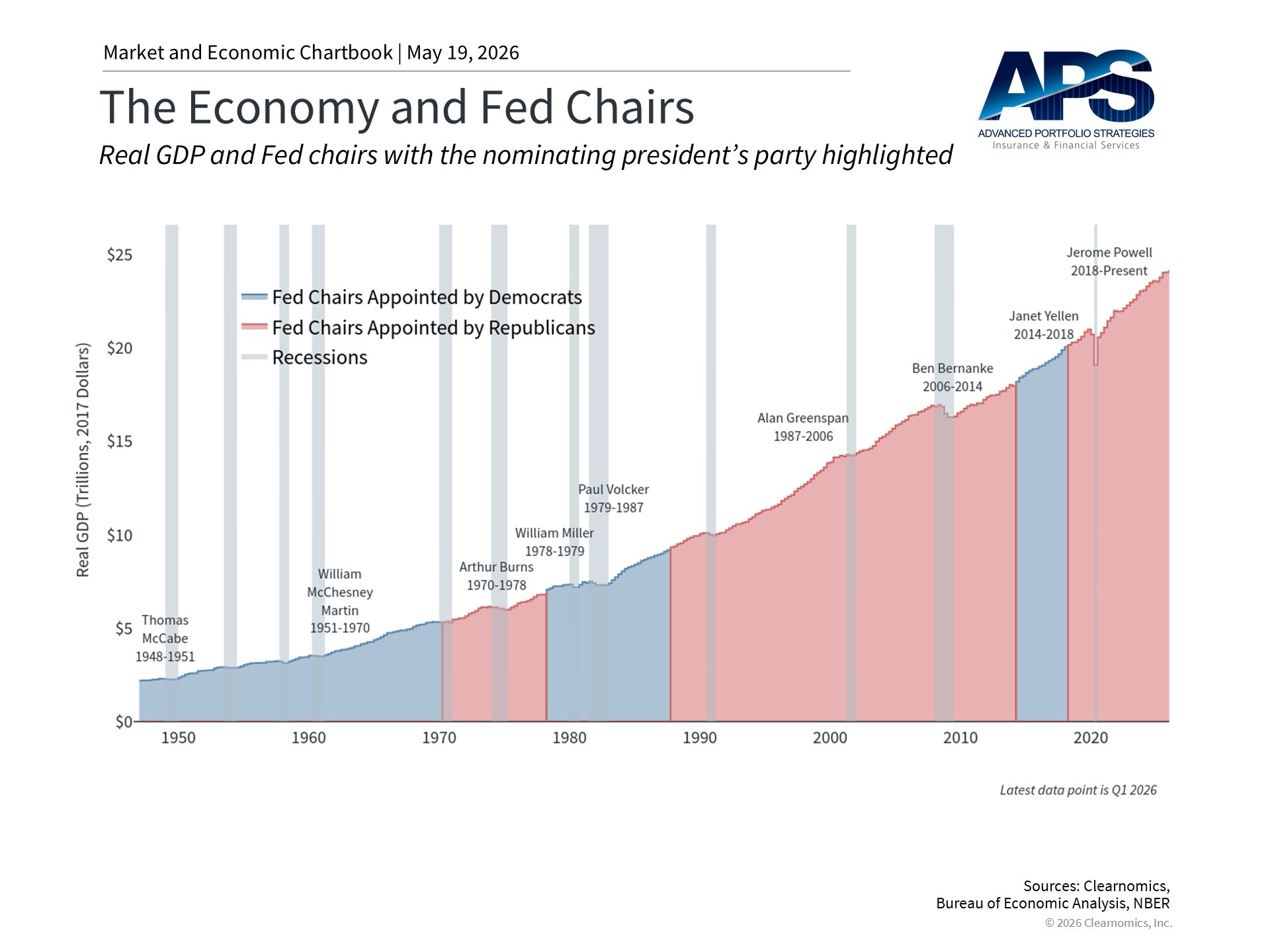

At the same time, we should not make Fed policy the entire investment thesis. The Fed matters, but it does not control everything. Over time, markets are driven by corporate earnings, productivity, innovation, demographics, fiscal policy, and the resilience of the economy.

For portfolios, the key is not to predict every Fed decision. It is to build portfolios that can handle a range of outcomes: persistent inflation, slower growth, changing rate expectations, and periodic volatility as markets adjust to a less interventionist policy backdrop.

We are watching several areas closely:

1. Whether inflation continues to move toward the Fed’s target or remains sticky.

2. How the bond market responds, especially longer-term Treasury yields.

3. Whether the Fed can reduce its balance sheet without creating liquidity stress.

4. Whether corporate earnings can hold up if borrowing costs remain elevated.

5. Credit conditions for consumers and companies.

6. Whether market prices begin to reflect fundamentals more than policy support.

The bottom line is that a Fed with greater focus, discipline, and credibility could be positive over the long run. Markets function best when capital has a real cost and risk is priced honestly. But getting from a highly interventionist environment to a more normal one may not be perfectly smooth.

That is why we continue to emphasize diversification, quality, valuation discipline, income, and risk management. The goal is not to build portfolios around a single Fed forecast, but to remain resilient as policy, inflation, and market expectations evolve.

Sources:

- Clearnomics, “How the Fed Under Kevin Warsh May Impact Markets,” May 2026.

- First Trust, “Making the Fed Great Again,” Monday Morning Outlook, May 18, 2026.

APS Management Group, Inc. is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

APS Management Group, Inc. does not provide tax or legal advice; consult your tax or legal professional regarding your particular situation.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. We believe the information contained in this commentary has been obtained from sources that are reliable. This publication is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.